Celebrate ten years of Urban Omnibus and support ten more years of fresh, independent perspectives on citymaking with a donation today!

Celebrate ten years of Urban Omnibus and support ten more years of fresh, independent perspectives on citymaking with a donation today!

While Hurricane Sandy made real the devastating impact of coastal flooding, a bureaucratic change may bring catastrophe to coastal dwellers even before the next storm. A routine update to FEMA’s Flood Insurance Rate Maps, introduced in 2013 but yet to take effect, may make living in the floodplain an unaffordable future.

The National Flood Insurance Program was founded in 1968 and requires states to draw flood maps indicating areas that fall within the 100-year flood zone (which correlates to a one percent chance of flooding in any given year). While municipal participation in the program is technically voluntary, mortgage lenders demand flood insurance for homeowners in the floodplain. So when the floodplain suddenly and radically expands — as it did when FEMA issued the 2013 update, thirty years after the last update — homeowners with federally-backed mortgages were in a bind. From Des Allemands, Louisiana, to Syracuse, New York, residents were told that they would need to raise their homes on stilts or suffer flood insurance penalties usually in the thousands of dollars.

The flood zone maps aren’t necessarily meaningful for demonstrating actual risk: The City of New York has appealed to shrink the flood zone, claiming the maps overestimate the size of the floodplain, while climate scientists say the zone should be much larger since the maps don’t take climate change into account. But as official documents, they are very powerful. New York City has more residents living in high-risk flood zones than any other U.S. city, most of whom are working- and middle-class. It also has a much denser building stock — one that can’t always be lifted on stilts.

Henry Grabar takes us to Canarsie, a southern Brooklyn neighborhood with long rows of two- and three-story attached brick houses where the rising insurance premiums might be a greater immediate threat to homeowners than the rising seas. Canarsie’s situation offers a lens into the uncertainties of adapting row houses and other urban building types in the flood plain, and the new questions climate change poses there: Whose responsibility is it to protect — and pay for — coastal dwellings, and if we stay by the seas in the face of certain sea level rise, what will that look like in the years to come? –E.S.

On a late summer afternoon, Canarsie is serene. A girl teaches her brother to skateboard in the street. Kids play Twister in a driveway. Brooklynites are outside, watering the little lawns that front the brick duplexes, tinkering with their cars, laughing in the shade of a plastic canopy. Rows of gnarled London Plane trees shade the streets; sunflowers strain towards the light. Down on Canarsie Pier the fishermen’s talk gets lost in the wind.

It’s an anomalous place: a safe Brooklyn neighborhood where a decent house can be bought for a few hundred thousand dollars. The homeownership rate is nearly 50 percent, nearly 20 points higher than the city average. This is a place where immigrants put down roots; where families buy their first homes. The population has changed, from Italians and Jews to African-Americans and Caribbean-Americans. But Canarsie retains its promise as a haven for the middle class, and for those who aspire to get there.

It is also in a difficult spot three times over. First, the 2007 subprime loan and foreclosure crisis hit Canarsie, with its many low-income homeowners, about as badly as any neighborhood in the city. Then, in 2012, the area was hammered by Hurricane Sandy, which damaged 83 percent of homes in Canarsie and neighboring Flatlands, according to the Department of Housing and Urban Development, and left the average homeowner with a $30,000 bill. Now, Canarsie finds itself — like many coastal communities — newly included in the Federal Emergency Management Agency’s 100-year flood plain, a designation with huge ramifications for homes and homeowners.

Canarsie’s struggles in the last decade aren’t atypical for a coastal American neighborhood, except for one thing: The building stock here is composed largely of row houses and semi-detached housing. Over 70 percent of Canarsie’s homes are connected on one or both sides. Protecting these homes from inundation, and dodging elevated flood insurance premiums, requires a new architectural playbook.

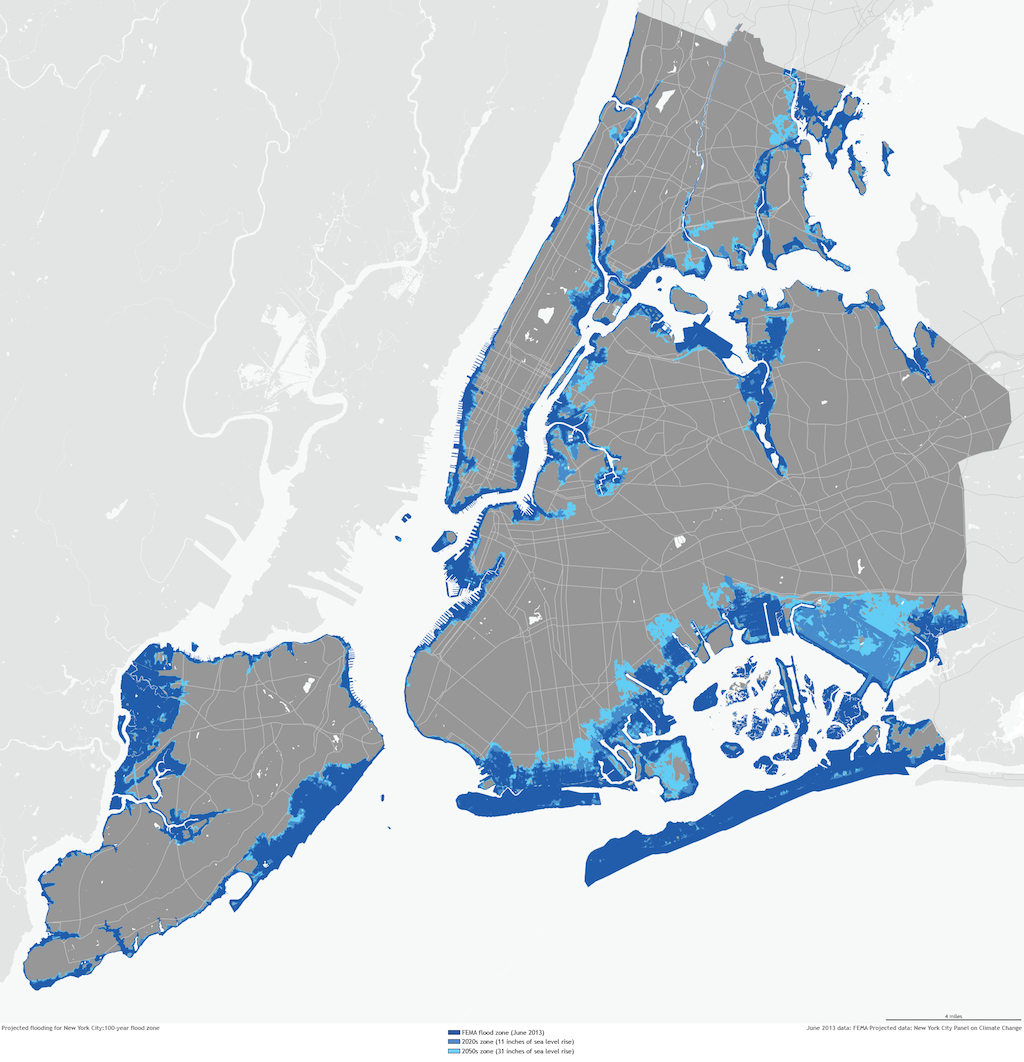

FEMA flood maps are supposed to help buyers, builders, and insurers determine risk. They guide both local building codes and the National Flood Insurance Program. But they have traditionally affected only a handful of New York City’s coastal residents. The last time FEMA released a flood map for New York City, in 1983, only the very edges of Canarsie were in the 100-year flood zone.

When FEMA revised its Preliminary Flood Insurance Rate Maps in 2013, as part of a routine update unrelated to Sandy, the agency raised the Base Flood Elevation, or BFE, which determines flood insurance rates. The number of New York buildings in the Zone A (high-risk) flood plain doubled, to 71,500. In Canarsie, the change was more dramatic: The number of structures in Zone A rose from about two dozen to 5,000, about two-thirds of the neighborhood. New York City says FEMA’s new maps exaggerate the flooding risk, and along with scores of other coastal communities and organizations, including the Port Authority of New York and New Jersey, has prepared its own countervailing analysis to dispute the agency’s maps, an argument that could wind up in court.

But if FEMA’s preliminary maps are officially adopted — the city’s appeal, filed last year, may take years to resolve — a wave of bank-breaking flood insurance premiums will wash over Canarsie’s low-lying row houses. Buildings with habitable space below the BFE will be subject to thousands of dollars a year in premiums for flood insurance, which is required for Zone A homeowners with FHA-backed mortgages. A FEMA fact sheet from 2012 estimated that $250,000 flood insurance coverage for a house whose living space started four feet below the BFE would cost $9,500 a year. In a neighborhood where the median household income is about $55,000, that would be an overwhelming blow.

The alternatives to the debilitating premiums aren’t much more appealing: rebuild upwards, abandon residential space below the flood line, or sell.

Unlike flood-prone detached homes in Gulfport, Biloxi, Norfolk, or Suffolk County, Canarsie’s houses can’t be raised, corner by corner, on supersized car jacks for $70,000. They have to be rebuilt, either by adjusting floor heights inside the structure or by making the lower level flood-ready and replacing that lost square footage with an added floor on the roof. Either way, it will be expensive. Not everyone can afford such a major construction project. Homeowners who convert low-lying rooms away from residential use could lose half their living space. The alternative to that is abandoning a lower-level unit entirely, along with the rental income it may generate. Or, of course, leaving.

“You can’t physically raise these houses,” said Alan Maisel, the councilman who represents most of Brooklyn’s Jamaica Bay coastline, when I visited his Flatlands office recently. “They had a guy from the Gulf Coast come after Sandy and he said, ‘You’re going to have to raise all these houses.’ And I said: ‘Have you driven around the neighborhood? Have you seen the kind of houses we have?’”

Canarsie is a preview of a battle between flood readiness and financial ability, which, as the seas continue to rise, will soon advance to most East Coast communities. It illustrates the unique challenges that new flood risks pose to New York’s super-dense building stock. And it reminds us that that both geography and economics are determining who will be the first climate change refugees. Maisel believes the new flood maps will place an existential burden on the area’s homeowners. “If the flood maps pass,” says Maisel, “I suspect large areas of Canarsie will become uninhabitable.”

Canarsie, a square of Brooklyn bounded by salt water on three sides, was settled for its easy water access. Long before the train crossed Jamaica Bay, the neighborhood served as transfer point for Brooklynites bound for the beach. Brooklyn’s Rockaway Parkway, which runs through the heart of the neighborhood, led to Canarsie Landing, where ferries departed for the peninsula.

Modern-day Canarsie, home to nearly 90,000 people, is the result of two discrete periods of intense construction. Metropolitan settlement came to the railhead during New York’s great housing boom of the 1910s and ‘20s, and clustered in the narrow rectangle of high land between Remsen Avenue and Rockaway Parkway, around the trolley lines. Then, in the 1950s and ‘60s, developers filled in the marshy land along Fresh Creek, to the northeast, and Paerdegat Basin, to the southwest. Blocks of low-slung brick homes sprawled towards the water, often with bi-level entrances and garages. The area was an outpost of white flight in the ‘50s; then, in the ‘90s and 2000s, Canarsie, like Bedford-Stuyvesant and Brownsville before it, gained a black majority. The neighborhood has the city’s greatest concentration of public workers, and a median income slightly above the city average.

When Sandy came, water surged in from the bay, the creek, and the basin. It pushed up through storm drains. In just a few hours, water in basements and ground-floor apartments was up to the windows. Thousands of people lost their cars, record collections, furniture. Residents couldn’t believe it happened. And many believe it could not happen again.

“These are not beachfront homes,” said Carl Palmer, a Canarsie resident of 20 years who lives on Avenue L near the Spring Creek marshland. His basement rooms had water up to their windows. “That’s once in a lifetime, that’s never going to happen again.”

Many of his neighbors agree.

After Sandy, and after the publication of FEMA’s revised preliminary flood insurance maps, the city modified its building code to require builders here to design for a 100-year flood. That meant no residential space can be located below Base Flood Elevation, which is ten feet above sea level in Canarsie. The building code changes haven’t impacted many residents yet. Thousands of units were grandfathered in; homeowners aren’t required to get up to code unless they are conducting major renovations.

But if virtually no houses here have been brought up above the BFE, architecture is also to blame. “FEMA really hadn’t addressed this typology before we started looking at it,” said Eugenia di Giralomo, a former urban designer at the Department of City Planning. The agency’s guidelines to date deal nearly exclusively with the detached single-family home common to most of the rest of the country.

“A lot of FEMA’s work is where buildings were far apart,” added Daphne Lundi, a flood resilience planner at DCP. “After Sandy was the first time there needed to be a standard of retrofitting where you have something attached to something else. The architecture and engineering present new challenges.”

In 2014, city planning made an effort to fill the gap, publishing a guide, “Retrofitting Buildings for Flood Risk.” It’s a sobering, design-based analysis of the changes that New York must undergo — if not in the next few years, then at some point soon afterwards — to adapt to flood risk and climate change. About 45 percent of the city’s at-risk buildings are detached, meaning they fit neatly with FEMA guidelines. Conversely, half of all at-risk units are in buildings of more than six stories, where adaptation cost is less relative to the building’s value. In the middle is a slice of semi-detached and attached housing where repairs are complex, expensive, and unprecedented.

The report is frank: If you have occupied living space below the BFE, all but the most expensive retrofit options could entail losing up to half your home’s square footage. Houses with ground-floor garages are the lucky ones. The city’s case study for the row house is a home where two-thirds of the residential space lies below the line.

A full-budget retrofit of a row house involves transferring the ground floor to non-habitable uses, installing flood vents, raising utilities like the boiler, and re-building the residential capacity on top of the building. That’s not a structural concern; many row houses can bear an extra floor. But it is expensive (adding a floor alone could cost $100,000), complicated (living space disappears when landlord and tenant don’t both have street access), and not particularly pretty.

Steve Lampert is a Canarsie old-timer. He grew up here when the kids had clubhouses in the marshlands, and the L train still had a grade crossing. Like most people here, he recalls Sandy as a cataclysmic event. The bottom story of the row house he shares with his wife was flooded. Water pressure from outside kept the doors from opening. The pair would have drowned if not for an interior staircase, he said.

Sandy killed the colonnades of trees that shaded the block. It killed the garden Lampert had tended for migratory birds. But he can’t come around to the idea of everyone transferring street-level living space to their roofs. “If there’s any kind of architectural aesthetic, it’s that no one has a third story,” he said, looking down his block of row houses. Canarsie’s three-story blocks are just as uniform. Uniformity is one of the area’s great charms.

If the FEMA flood maps — which will require retrofits, lost space, or force high insurance premiums — are approved, the issue will be more than aesthetic, though. “Canarsie is one of the most affordable neighborhoods in Brooklyn,” says Jean-Paul Ho, a broker at Brooklyn Real Property who owns property in the area. “The price outweighs concern about raising and rebuilding. Canarsie had never been flooded before Sandy happened, which is why some people think this is once in a lifetime.”

Councilman Maisel, who lives in Marine Park, isn’t naive about the threat that climate change poses to his district of 160,000 people. Maisel knows that DCP and FEMA have worked to establish a prototype for “raising” the row house. But he worries that people couldn’t afford it. (Some federal grants are available for floodproofing.) Like many people in Canarsie, he said the solution was a Jamaica Bay surge barrier. A policy putting the cost of adaptation on the area’s low-income homeowners wouldn’t just jeopardize their finances; it would also deter newcomers. The FEMA maps won’t take effect until New York’s appeal is resolved. But many climate scientists say the agency’s calculations, which don’t account for future sea level rise, already underestimate the risk. Another Sandy would be a disaster for a neighborhood that is no more prepared than it was in 2012. But insurance premiums and renovation mandates could be a disaster, too, one that plays out not in Canarsie’s flooded streets but in its savings accounts — and in similar neighborhoods across the city.

“If the amount of money for flood insurance is enforced, they can’t afford it,” Maisel said of Canarsie. “If you add on several thousands in flood insurance, this whole neighborhood is going to be neglected and abandoned. There will be fire sales. If I were living in Canarsie, I’d seriously consider moving to Crown Heights.” That neighborhood has some of the highest ground in Brooklyn.

The views expressed here are those of the authors only and do not reflect the position of The Architectural League of New York.

Comments