Last year’s mayoral election vaulted the growing need for new affordable housing to the center of discussion over New York City’s future, and Mayor de Blasio released an ambitious plan earlier this year, pledging to create or preserve 200,000 units in the next ten years. But public discussion of the plan thus far has almost exclusively focused on the creation of new housing rather than the preservation of existing units. In a city where land for new construction is at a premium, maintaining assets already in place is crucial. According to a Community Service Society report released in January, the city lost 385,000 units of affordable housing between 2002 and 2011, far outpacing the 165,000 units that the Bloomberg administration aimed to create and preserve. If the loss of affordable homes continues at this rate, plans for new construction will fail to replace diminishing supply, let alone meet our growing city’s demand for more affordable housing.

Units built under Mitchell-Lama, a State program signed into law in 1955 to spur the construction of middle-income housing, are one source of affordable housing particularly vulnerable to loss. In exchange for a low-interest mortgage rate and property tax exemptions, Mitchell-Lama units held affordability restrictions for their first 20 years. Thereafter, the real estate companies that owned rental complexes or the shareholders that owned Mitchell-Lama co-ops have the decision to remain in the program and retain the restrictions, or buy out their mortgage and release the units to valuation and sale on the open market. 271 properties, containing 139,428 units, were developed in New York City through Mitchell-Lama. As of November 2013, only 78 developments, containing 32,900 units, remained in the program. The rest have chosen to opt out.

Charles Chawalko, a recent graduate of Parsons’ Design & Urban Ecologies program, is a resident of Southbridge Towers, a 1,651-unit development that remains in the program. But as he explains below, his cooperative is in the midst of a decision over whether it will join the majority of Mitchell-Lama buildings and leave. To residents of Southbridge Towers, the vote over whether to opt out of Mitchell-Lama transcends the citywide conversation on affordable housing, replete with numbers, prices, and policy intricacies. The upcoming vote will have major personal repercussions for their homes, financial futures, and community culture. And as Chawalko’s account foregrounds, the debate underway in Southbridge Towers highlights the complexity of how we value where we live and the importance of transparent dialogue and fair governing processes. –J.T.

Southbridge Towers | Photo by Jonathan Tarleton

A community of over three thousand residents living and working in affordable high-rises, people who banded together to form a community in a barren landscape decades ago when the city was hardly a shining beacon of prosperity. As time flies by, a war of words erupts over the community’s future and how it governs itself. Friends and neighbors become enemies, conflict commonplace, and truth a scarce commodity in everyday life…

I am not describing J.G. Ballard’s High-Rise. This is the story of my home as it undergoes a battle for its future. Southbridge Towers is an affordable housing complex built under New York’s Limited Profit Housing Company Act, an affordable housing program more commonly known as Mitchell-Lama and lauded by both politicians and activists. Today the program contends with internal and external pressures that lead to the privatization of its buildings, or to owners and governing bodies at least considering it. During my graduate work in Design & Urban Ecologies at Parsons, I looked at the impact of the redevelopment of Lower Manhattan on the complex where much of my family has lived since construction, hoping to understand and describe the motives behind a push to privatize this middle class haven. Like many residents, I feel deeply connected to these buildings and the very program that supports their operation, and I strongly believe that residents are entitled to a transparent process that accurately informs them of any decisions affecting the complex’s future, particularly the privatization debate currently underway.

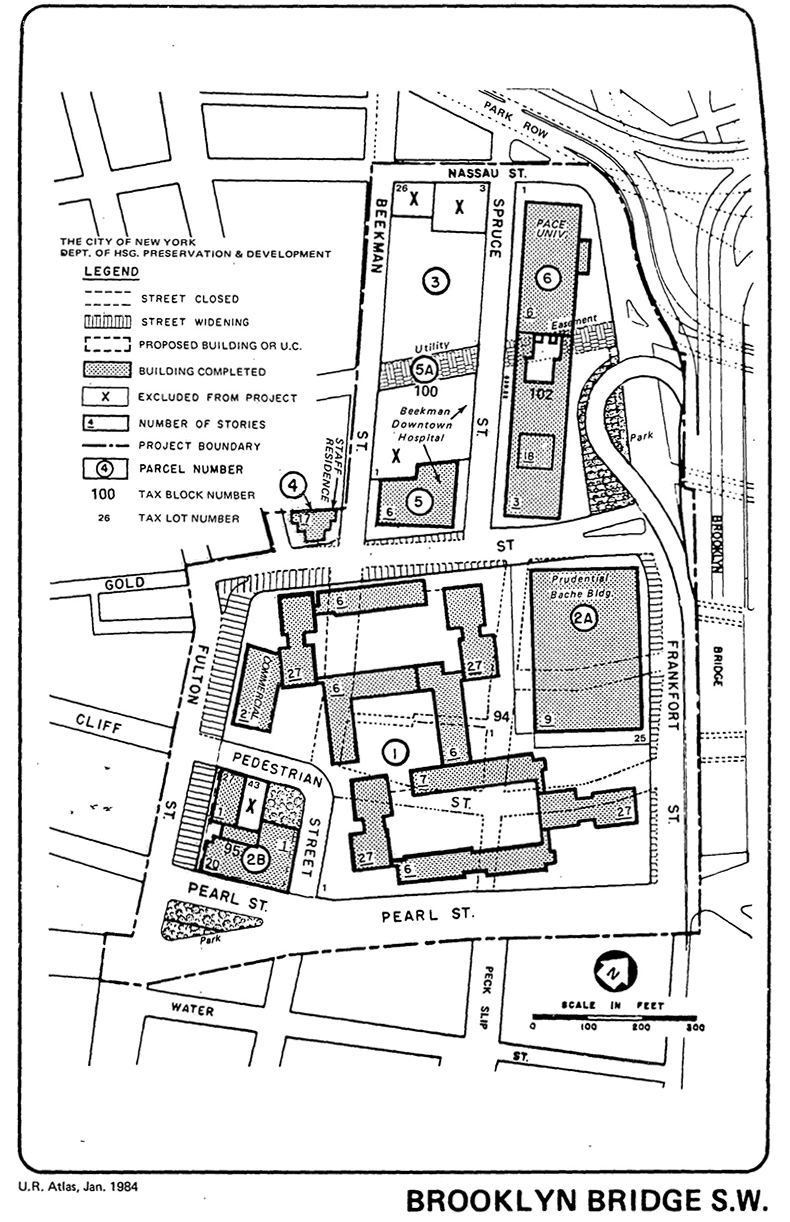

Map of the Brooklyn Bridge Southwest Urban Renewal Area plan; area (1) is Southbridge Towers. | Image via Urban Reviewer

Located in the South Street Seaport area of Lower Manhattan, Southbridge Towers (SBT) was born out of the Brooklyn Bridge Southwest Urban Renewal Area, a designation laid upon a rather dark and congested stretch of industrial waterfront in 1964. The urban renewal plan aimed to create a middle-income community that could tame and transform the neighborhood, boosting property values and fashioning a more modern, healthier tax base for the city. The State, through Mitchell-Lama, provided a low-interest mortgage rate and property tax exemptions to spur the development of the complex, which is organized as a limited-equity, shareholder-owned cooperative. No real estate company owns the complex, as is the case with Mitchell-Lama rental properties; instead, each unit holder purchases equity in the cooperative, and in lieu of selling the apartment when they wish to leave, the cooperative pays the departing resident for his or her equity plus accrued interest. Management and operating procedures are governed by a board of 15 directors who reside in SBT, designated in annual elections for five board seats with three-year terms, plus an observing member appointed by the State’s Division of Housing and Community Renewal (DHCR).

The surrounding area of Lower Manhattan has radically evolved from the 1950s to the 2000s. Once maligned as an industrial and corporate ghost town, it is now one of the city’s fastest growing neighborhoods. Massive developments, like the World Trade Center and Battery Park City, and newly invigorated commercial, residential, and public projects have reshaped SBT’s surroundings into a 24/7 neighborhood. During these decades of transformation, the seeds of a campaign for privatization began to be sowed. SBT’s land, sold to the complex by the State for $1.3 million dollars in 1967, is now worth far more, approaching eight figures. Shareholders originally purchased apartments for equities ranging from $5,000 to $28,000 over the last four decades, but price estimations for the apartments on the open market skyrocket to between $500,000 and $1,000,000 depending on the size and placement of the unit. These shifts have altered the perception of what SBT means to its residents. Do SBT’s apartments provide affordable shelter or are they commodities? This question divides residents into two groups currently fighting over the future of SBT.

Southbridge Towers courtyard | Photo by Jonathan Tarleton

Privatization, reconstitution, dissolution, and demutualization: these terms all refer to the same process of removing the cooperative from the oversight of DHCR and reclassifying it as a private market cooperative whose apartments can be sold on an open market. The concept of “privatization” is controversial, subject to a philosophical disagreement over the intentions and goals of Mitchell-Lama. Was the program designed to be a time-limited operation should the then “housing crisis” be solved in 20 years, the initial term of the program after which a development could opt out? Was it a program to give the middle class the opportunity to afford a home? When the privatization clauses of the enacting law were drafted, did legislators intend to treat cooperatives and rental properties the same? Each of these questions has multiple answers, depending on your views of housing, economics, and real estate.

There are now two scenarios for Southbridge Towers: remain in the Mitchell-Lama program with affordability provisions intact, or leave it, freeing the complex from government oversight and giving shareholders the right to sell their units in the open market. Both have benefits and disadvantages.

Southbridge Towers (bottom right) sits in front of the then under-construction One World Trade Center (left) and New York by Gehry (right), 2012 | Photo by Mark & Andrew Busse

Mitchell-Lama cooperatives are only required to pay a percentage of gross monthly maintenance charges back to the City or State in lieu of actual property taxes, insulating the developments from the fluctuations of the real estate market. Shareholders’ monthly maintenance charges are below the city’s average, but there is an additional surcharge should you make beyond the income range set by the government. The complex has access to no-interest repair loans to finance any needed upkeep or capital improvements, as long as the complex stays in the program for 15 or 30 more years. Shareholders are not allowed to sell their units freely; instead, they must return them to the cooperative for their initial equity plus accrued interest.

If the complex were to be privatized, proponents believe that the cooperative can remain affordable and financially viable by collecting a flip tax or transfer fee when units change hands. For first time transfers, the cooperative will collect 28% or 33% in fees, pending the outcome of a lawsuit involving Trump Village, a co-op in Brooklyn that recently left the Mitchell-Lama program. For future transfers, the fees would only be 2.5%. Privatization advocates believe that affordability can be maintained if a minimum of 50 units are sold or transferred each year. Maintenance charges would be increased to cover additional monthly demands, among them newly collected property taxes. Those who cannot afford the new charges could remain in the complex with their apartments as long as they become renters, their charges pegged to the Rent Guidelines Board’s annual decision on rent increases, never to exceed five percent.

Cover and introduction of a 1980 guide distributed to Southbridge Towers residents by the cooperative’s Board of Directors | Images via Charles Chawalko

Growing up in Southbridge Towers, privatization was mentioned frequently, but its policy intricacies were often beyond me. The idea of leaving the program meant losing the security of the shelter, affordability, and other safeguards that the program provided for my family and neighbors, but it also held the allure of a major source of new money. The first buds of possible privatization grew in the 1980s, but little came of them. The diverse group of individuals that made up the Board of Directors through the 1990s saw the Mitchell-Lama program as a refuge for working and middle class individuals that were increasingly displaced by a lack of affordable, modern housing stock. A strong sense of community spawned a senior activities center, a lending library, community groups celebrating the many nationalities represented in the complex, and other amenities.

Thirty years after the first residents moved in, a second and third generation of shareholders took over governance of the cooperative amid a subtle socioeconomic shift in the complex. The economic security, safe environment, proximity to white-collar and government jobs, and the economic ability to access educational opportunities that Southbridge Towers provided meant those residents were often better off financially than their forebears. The complex was primarily seen as a haven when original shareholders needed to find a home; now more economically secure, some began to evaluate their apartments as an economic asset, a commodity. Some residents had purchased second and third homes while Southbridge Towers remained their primary residence, making the option of cashing in on their unit more feasible.

Southbridge Towers Management Office | Photo by Jonathan Tarleton

Between 2001 and 2004, individuals interested in exploring privatization started to win seats on the board. The issue was not a major part of their platform at first; their election was seen as a prudent weighing of shareholders’ options through a feasibility study. But privatization soon became the dividing line on the board and in the complex. A group of board members focused on privatization formed Southbridge Rights, Inc. in 2004, effectively creating a political party in an effort to direct internal cooperative politics. Previously, the board had been a non-partisan body; now, elections come down to whether or not a voter is for the view of privatization promoted by Southbridge Rights. Rules of open board meetings were modified to require pre-approval before residents could raise new issues, creating an atmosphere in which some shareholders with opinions different from Southbridge Rights’ policies, which hinged largely on pushing privatization, felt silenced.

Southbridge Rights’ rise to power correlated with an increased use of proxy ballots in annual elections. While these ballots are legal under cooperative rules, shareholders used them sparingly before 2001. Since, elections have routinely been decided by blocs of proxy votes, and candidates from Southbridge Rights routinely occupied 13 or 14 of the 15 seats. This shift in power appears to point to a significant effort to drive votes. Some shareholders believe that Southbridge Rights has employed a strategy of targeting elderly shareholders and illegal subletters to cast proxy votes in the group’s favor, prompting DHCR and the Attorney General’s office to modify the development’s voting procedures by directly sending shareholders uniquely bar-coded proxy ballots to curb potential voting abuse.

Southbridge Towers promenade | Photo by Jonathan Tarleton

In November of 2005, a complex-wide referendum approved the creation of a feasibility study to explore privatization and allocated $25,000 towards its production. The study was released in October of the following year, and a Red Herring — the legal term for a draft of an offering plan for privatization — was submitted to the State’s Attorney General’s (AG) office for review. Privatization procedures for other Mitchell-Lama developments have taken upwards of two years to reach a final vote. This would not be the case with SBT. The Red Herring was at the AG’s office for over seven years undergoing revisions, edits, and clarifications. At one point, it was publicly reported that there were over 300 deficiencies with the plan. During this period, the Board of Directors, under a gag order required by Attorney General and DHCR rules, consulted with the AG’s office to clarify the deficiencies, and SBT Cooperators for Mitchell-Lama, a group against privatization that’s been operating in the complex for over a decade, worked with the AG to make the plans as transparent as possible.

In April of 2014, the Red Herring was accepted by the Attorney General, thus becoming the Black Book, the legal term for an approved offering plan. Exceeding nine hundred pages, this tome of complex legal, accounting, and engineering reports requires professional training to comprehend. The development’s attorneys and the Attorney General’s office recommended that shareholders seek out their own attorneys and accountants to properly evaluate the proposal, an expense that not all shareholders are able to handle. And while the Black Book seemed largely to mirror the Red Herring, significant alterations were made that went unexplained to shareholders upon delivery. For example, succession rules were rewritten. The Red Herring exempted many familial relations from transfer fees when taking over an apartment of a deceased relative, but the rules in the Black Book require the fee for anyone who is not a spouse or adult child of the relative and give the board the right to approve or deny such a transfer. The combination of the plan’s complexity and unexplained changes have made the process particularly inaccessible to the average shareholder. The significant impacts that privatization would have on each shareholder require a transparent and explanatory process. Instead, the Board has made little effort to explain the benefits or the drawbacks of the plan, and efforts to enlighten or clarify its provisions are met with accusations of partisanship.

Two of the three Southbridge Towers | Photo by Jonathan Tarleton

As a vote on privatization came into view with the issuance of the Black Book, members of the Board of Directors increasingly avoided public appearances while discussion in the cooperative grew more heated. I spent time with the Southbridge Towers Shareholders Association, a group created in 2012 in a response to the growing insularity of the Board. The Association aims to be an advocate for facts in the privatization dispute, frequently making requests to both the development’s management and oversight officials, through Freedom of Information Act requests and personal letters and petitions, to gain more clarity on SBT’s daily operations and the privatization process.

Despite its intention to provide unbiased analysis of the issues and to empower shareholders to make an informed decision, the Shareholders Association faces constant criticism that it is a partisan organization in favor of staying with Mitchell-Lama. Concerned Shareholders for Transparency, a group led by pro-privatization residents unaffiliated with Southbridge Rights and the Board of Directors’ policies, has attempted to counter the Association’s explanations, claiming they are scare tactics. One’s views on housing, economics, and real estate are the lens through which the privatization offering plan is considered, and pro-privatization advocates see anything critical of privatization or the Board’s policies and action as misinformation. An anti-privatization resident will highlight the Special Risks section of the Black Book, which details a list of possible financial perils that could befall what is currently a fiscally healthy cooperative. A pro-privatization resident will claim those are only minor concerns, just legal boilerplate that lawyers include to cover every eventuality. But what is more troubling to me is an attempt to mischaracterize Southbridge Towers’ current manifestation as unsustainable. Pro-privatization groups try to undermine resident confidence in the development as a permanent and viable institution under Mitchell-Lama, claiming that continual maintenance increases make the arrangement financially precarious or that the complex isn’t guaranteed its place in the program.

Southbridge Towers | Photo by Jonathan Tarleton

In accordance with Mitchell-Lama rules, an informational session by the Board of Directors and the cooperative’s attorneys, accountants, and consultants must be held before a vote on privatization can take place. Though not intended to provide one-on-one professional counsel, the meeting is meant to explain the complexities of the plan so as to allow residents to vote knowledgeably. That meeting — the only public information session of its kind — happened on July 29th, and while the Board of Directors touted it as a success, it was not considered as such by the Attorney General’s office when a recording of the session was brought to their attention. Deeming that consultants at the session had overstepped the bounds of the Black Book in making certain comments, the AG required a second amendment to the offering plan that retracts two dozen statements made in the session. Problematic statements included that “a meteorite was more likely to hit us than the worst-case scenario happening,” which took the place of an explanation of the Special Risks section. Maintenance increases were referred to as “only X dollars more per room per month” to an audience including individuals with fixed incomes.

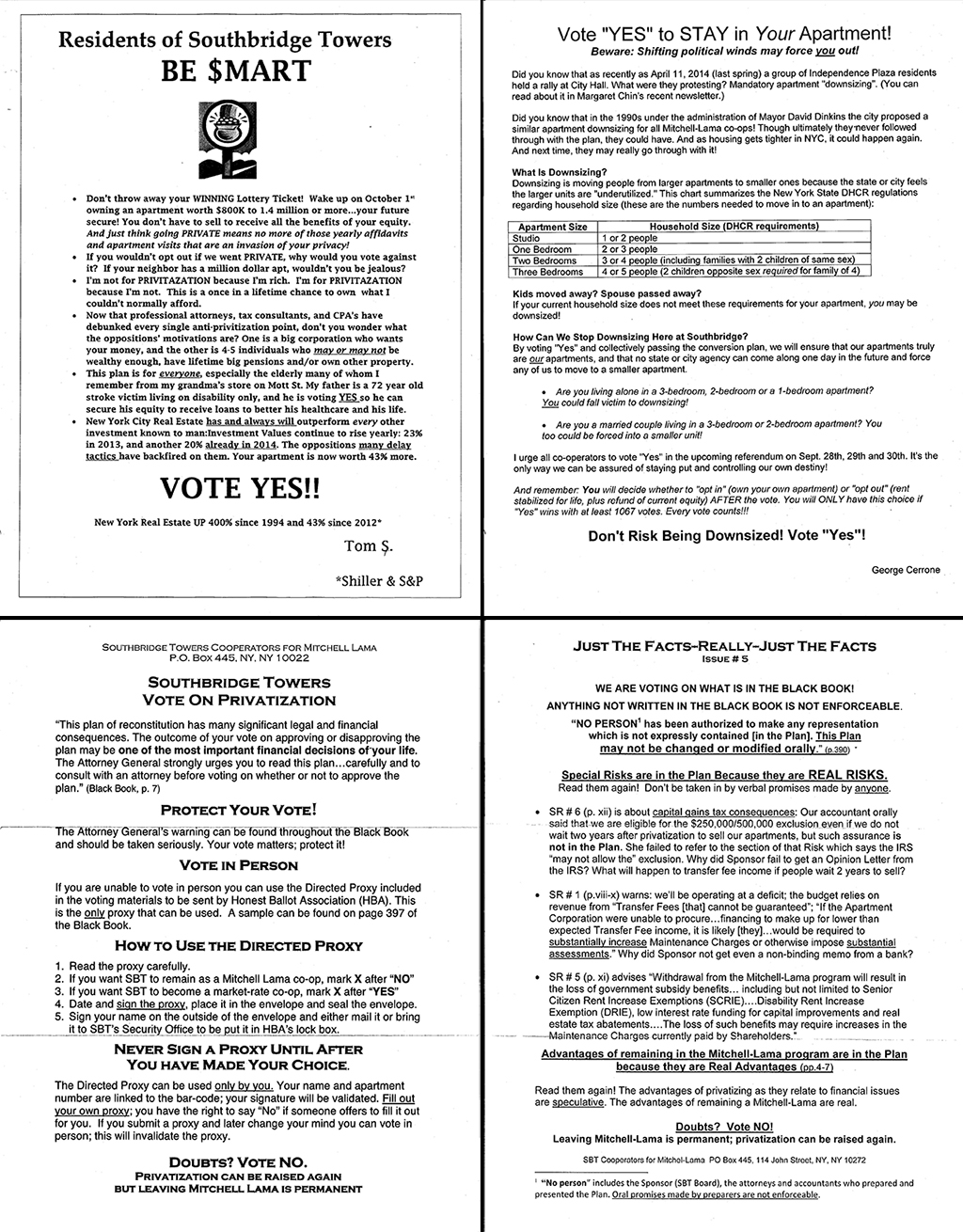

Flyers distributed by pro-privatization groups (top) and anti-privatization group SBT Cooperators for Mitchell-Lama (bottom) | Images via Charles Chawalko

There are only weeks left until the final vote on privatization at Southbridge Towers occurs, from September 28th through 30th, and it is apparent that this conflict is reaching its apex. Fliers are distributed daily to residents’ front doors. Some pro-privatization posters distort the debate by introducing issues that have no bearing on the current circumstances of Mitchell-Lama, like resurrecting the old idea that residents might be forced to move into different, smaller units if we stay in Mitchell-Lama despite the fact that a downsizing policy was explored by the State, then discarded, years ago. They continually make note of the “relative affordability” preserved in Seward Park Cooperative after its privatization, failing to note that Seward Park was developed by the United Housing Foundation, a federation of unions and non-profits, rather than through Mitchell-Lama. Anti-privatization fliers referencing Black Book clauses are circulated as well, including some with incorrect interpretations later corrected at Shareholders’ Association meetings. Disagreements over privatization have even led to verbal and physical violence; some neighbors fear walking through the courtyards will lead to squabbles on the matter. What was once a cozy complex working collectively to create a community downtown has turned into a battlefield of opinion dividing friendships and families. Perhaps J.G. Ballard’s High-Rise does provide some advice for this siege from within: “Living in high-rises required a special type of behavior, one that was acquiescent, restrained, even perhaps slightly mad.”

While this account might seem like a passionate, personal case, the outcome of Southbridge Towers’ privatization has ramifications for all affordable housing in New York. If the complex leaves the Mitchell-Lama program, New York would lose 1,651 units of permanent middle-income housing that cannot be recovered, the largest complex to privatize so far. Last month, over 50,000 people entered a lottery for 300 units in Penn South, a middle-income, limited-equity housing co-op in Chelsea. The importance of preserving each affordable unit we already have, and a healthy economic diversity in New York City, is clear. But the decision that Southbridge Towers’ residents face in the upcoming vote is ultimately a personal one. I have yet to make up my mind on the issue. But what I find most important is that every resident is able to make an informed decision concerning our complex’s future, as it has great ramifications for how we will live. Privatization can be voted down and explored again in the future, but once a development leaves Mitchell-Lama, it is a permanent departure. Whichever path residents vote to take, Southbridge Towers’ experience is a cautionary demonstration of the importance of a transparent and open discussion.

Looking down on the East River from New York by Gehry; two of the Southbridge Towers are to the bottom right. | Photo by Scott Beale