Series

Housing Brass Tacks

Reports from a series of informal conversations with scholars and experts engaging complicated topics in housing policy, hosted by The Architectural League.

We are celebrating 15 years — and counting — of stories that are deeply researched and deeply felt, that build a historical record of what the city has been.

Classifications, market values, assessed values, caps, abatements—the byzantine system of New York City’s property tax assessments is not merely complex, but is widely considered unfair and inequitable. George Sweeting, Deputy Director of the New York City Independent Budget Office (IBO), laid bare the myriad problems caused by a seemingly mundane facet of local governance in our 11th Housing Brass Tacks discussion. We used his talk as a jumping off point to untangle how property taxes work and why they matter.

The local property tax is the city’s single largest funding source and is “absolutely critical to the New York City budget,” explained George Sweeting. Property taxes will bring in a projected $26.3 billion this year; that’s 46 percent of all tax revenue, funding nearly a third of the mayor’s $84.86 billion budget — enough to fund the entire Department of Education, the largest item in the city’s annual expense budget. And with six percent annual growth projected over the next four years, it’s particularly valuable as a dependable revenue stream, stable even during recessions and economic uncertainty.

It’s also the target of widespread ire. The property tax is “probably the most resented form of taxation,” said Sweeting, with taxpayers taking a large hit all at once rather than in incremental paycheck deductions. “Dissatisfaction with the city’s property tax system is a near-universal complaint among New Yorkers,” according to the IBO. Criticized for its complexity, lack of transparency, and unequal burdens, the convoluted system seems to have no defenders.

Layers upon layers of complexity The byzantine steps of property taxation begin with assigning all properties to one of four tax classes: one-to-three-family homes (Class 1); all other rental buildings, condos, and co-ops (Class 2); utility company properties (Class 3); and all other commercial and industrial properties (Class 4). Then, assessors estimate the market value of each property, using prior year sales of comparable buildings for Class 1 properties, and income and expense statements submitted by most owners for Class 2 buildings. However, the assessment value is determined not by a property’s full market value but by a fraction of the value, arrived at by multiplying the estimated market value by the so-called target assessment ratio, which is six percent for Class 1 and 45 percent for all other classes. Then come a number of additional adjustments. For Class 1 properties as well as small Class 2 buildings, assessment caps limit the amount that the assessed value can increase annually. Meant to spare owners the burden of sharp yearly increases, these caps can lead to extremely low taxes in rapidly appreciating neighborhoods. In addition to creating large differences between similarly valued properties in different neighborhoods, the caps feed further social inequity: They benefit all residents in rapidly appreciating neighborhoods — even the wealthy and the newly-arrived — since there is no tax reset following sales and the low tax is passed onto new owners. These caps are “the real cause of much of the disparity” in taxation between similar-seeming properties, said Sweeting. For Classes 2 and 4, the Department of Finance (DOF) phases in changes to assessed value over five years, applying 20 percent of the change each year. A building could phase in multiple value changes in the same year, leading to a lot of confusion over the actual assessment as well as the need to issue multiple tax bills each year.

But that’s not the end of it. In an attempt to keep the share that each tax class pays consistent with what it paid in 1981, when a new tax law was adopted — a nonsensical practice, given how dramatically property values have changed since that time — the city employs a class share system. Today, Class 1 houses account for 46.9 percent of all market values in the city but pay only 15.2 percent of total taxes. “Certainly of the large tax systems in the country, we are by far the most complex,” concluded Sweeting. “And that’s not necessarily something to be proud of.”

A good taxation system should have the following qualities, said Sweeting:

The last is the only area where New York City excels, while the first two are particularly problematic. “You don’t want the tax burden to go down as ability to pay goes up,” said Sweeting. “But that’s what we have in New York.”

How we got here In 1974, a New York City couple with a vacation house on Fire Island filed a lawsuit, counterintuitively charging that the town was under-assessing its properties — including their own house — thereby leaving potential tax revenue on the table. The Hellerstein v. Town of Islip ruling decreed that the town had violated the state’s 1788 tax law by assessing single-family homes at a percentage of their value rather than the full market value; subsequently, assessments throughout the state would need to be for a property’s full value. The ruling sent policymakers scrambling, but according to the IBO, didn’t garner much progress: “After roughly six years of delay and sporadic debate, the legislature responded to the court decision by replacing the old law with one that allowed localities [New York City and Nassau County] to largely keep doing what they were doing.” The new statute (S7000A) took effect in 1983 and created the current property classification system that allows different types of properties to be taxed at different rates. Meant to maintain the existing distribution of tax burdens, homeowners still saw lower taxes at the expense of apartment and commercial property owners. Over the last 35 years, a series of band aids have been applied to fix various issues with the statute — exacerbating other issues in the process.

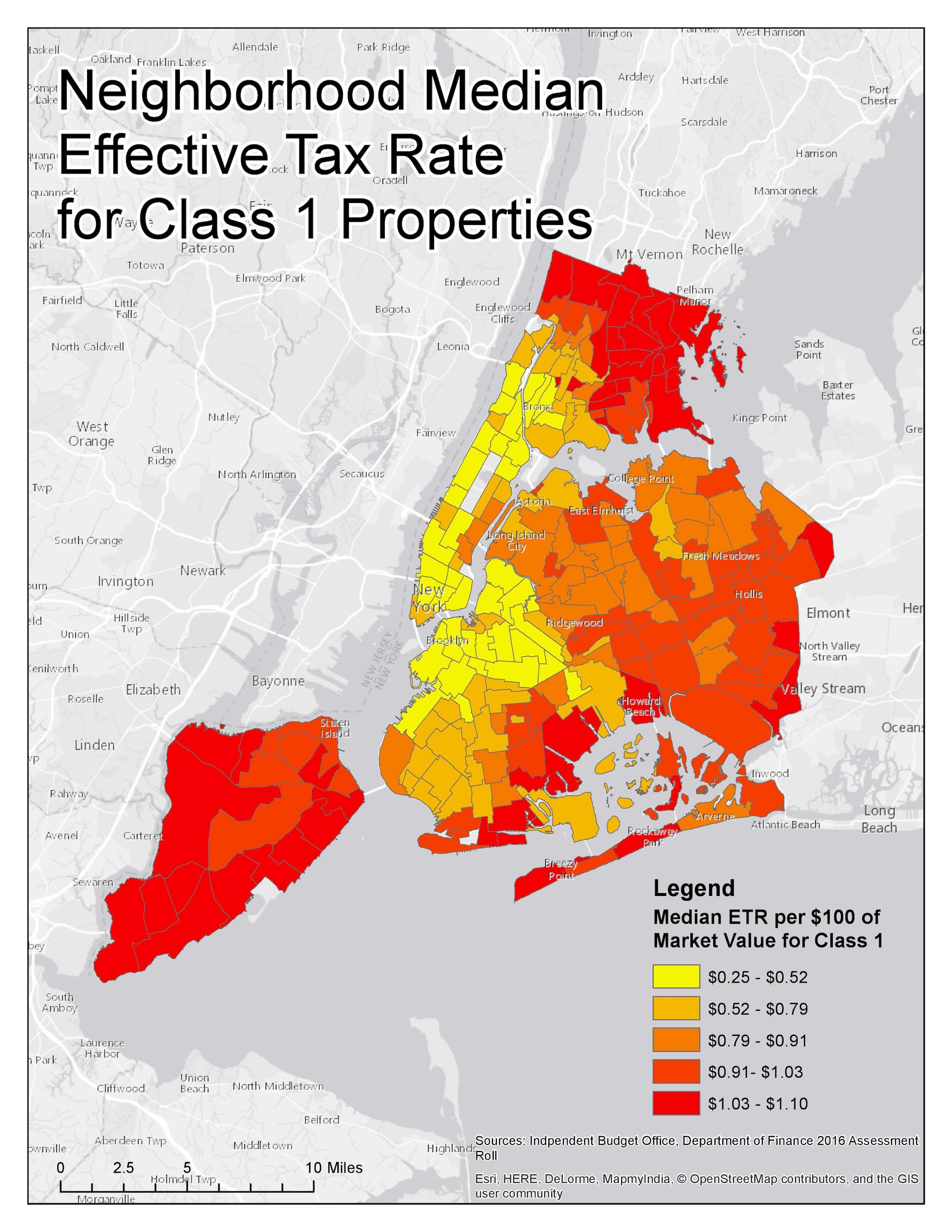

Geography matters in property taxes. If you live in a neighborhood seeing new development or experiencing gentrification, you are likely to benefit from the assessment cap for years to come. In 2016, two Staten Island council members asked the IBO to investigate what they perceived as inequities in how single-family homes on Staten Island were being taxed. They called out the disparity between a yellow clapboard row house on Dean Street in Brooklyn worth $1.7 million with a tax bill of $3,868, and a detached house on Falcon Avenue in Staten Island built in 2008 and worth $509,000 with taxes of $5,972. For every $100 of value, 474 Dean pays $0.23 in property taxes, compared to 554 Falcon’s $1.17. If all Class 1 properties were taxed at the target six percent rate, the effective tax rate should be $1.20 per $100 of market value. Instead, the city’s actual median rate is $0.90.

The IBO found no bias toward Staten Island but that the assessment cap benefits houses in rapidly appreciating neighborhoods — in the shadow of the Barclays Center, the yellow row house had quickly become very valuable. The newly built house is at another disadvantage, since older properties can capture the cap’s advantages over longer periods of time. According to a 2017 report from the Lincoln Institute of Land Policy, “The owner of a newly built home with the median value in New York City ($538,300) would face an effective tax rate about 50 percent higher than the owner of a median valued home built prior to 1981 despite their having identical values.” Staten Island has the highest effective tax rates of the boroughs — but that’s the nature of the system, not bias.

Tax Equity Now In April, a coalition dubbed Tax Equity Now filed a lawsuit in Manhattan Supreme Court charging that the city’s “aggressively regressive” property tax system discriminates against low-income and nonwhite homeowners and landlords. They are challenging both the disparities in the taxation of different property classes — rental buildings pay an effective tax rate nearly five times higher than one-, two-, and three-family homes — and between similar properties in the same class—such as our examples at 474 Dean and 554 Falcon above. There’s a strong race and class dimension to these disparities: renters have less than half the median income of owners ($45,753 compared to $92,352 in 2016) and two-thirds of renters are racial minorities, compared to less than half of homeowners. In addition, the owners that benefit from tax caps and condo abatements tend to be wealthier and whiter than the general population. The unlikely coalition behind the suit includes the Rent Stabilization Association, a trade group for landlords; civil rights organizations such as the NAACP and the Black Institute; advocacy groups like the Regional Plan Association and Citizens Housing and Planning Council; and major developers such as the Durst Organization and Related Companies. The lawsuit charges that treating different property owners differently violates both the State and US Constitutions; in October, five city councilmembers filed court papers supporting the suit — and against the city they represent.

Recall that co-ops and condos are Class 2 properties, and taxed as if they are income-producing properties. But as homeownership units, co-ops and condos don’t produce income. So to determine their taxation, assessors are compelled by state law not to value units by sales prices in the building, but look at the income produced by similar buildings in terms of age, size, and location. Often the closest comparables are rent-regulated buildings with below-market income, making co-ops and condos vastly undervalued. A recent report from the Furman Center identified 50 co-op units where an individual unit was sold for more than the DOF had valued the entire building. The IBO estimates that only 18 percent of the market value of condos is included in New York’s tax base. The valuation here is beyond convoluted — Sweeting termed it “all fiction.”

Already getting a good deal, condos and co-ops also receive an additional benefit. Since they, in theory, are taxed using the Class 2 assessment ratio of 45 percent rather than the Class 1 target ratio of six percent, in 1996 the city implemented a temporary stopgap abatement to get condo owners’ taxes more in line with homeowners’ taxes until a better solution was found — but it has been renewed every time it was meant to sunset. Today, the IBO estimates that the city is spending $300 million annually on the abatement, of which $200 million is “totally unnecessary” to achieve the stated purpose of getting co-op and condo taxes in line with those of Class 1 properties.

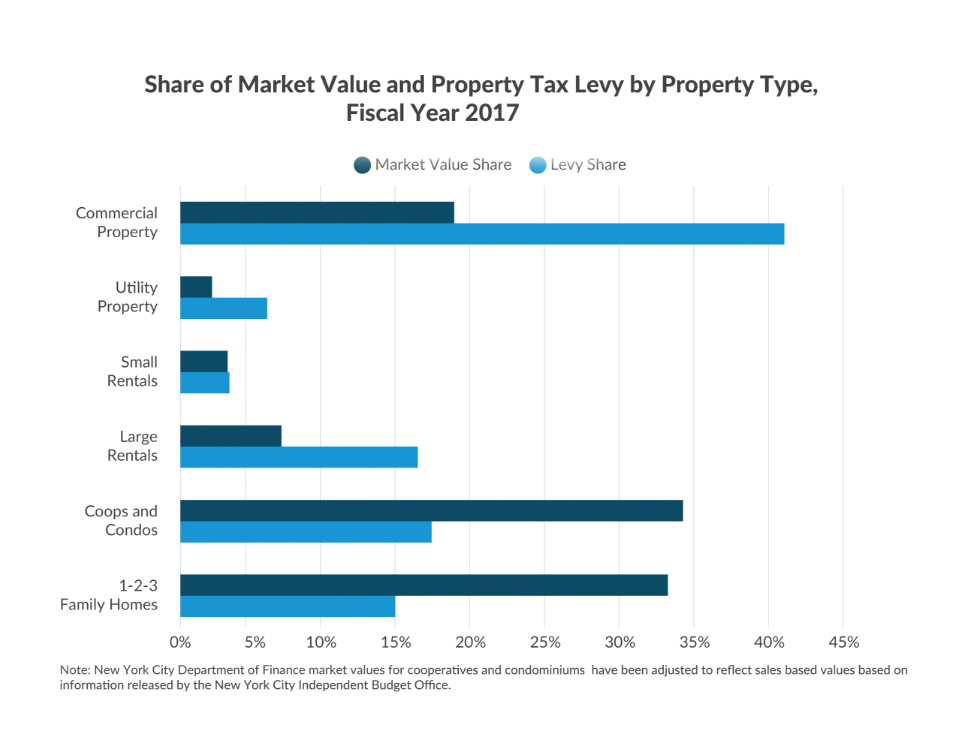

The losers: apartment buildings The effective tax rate for the city’s apartment buildings is nearly five times higher than the rate for one-to-three-family homes. New York’s apartment tax rate is a “major outlier” compared to other large cities and demonstrates “the degree of subsidy provided to homeowners at the expense of renters,” according to the Lincoln Institute report. Class 2 properties make up 24.5 percent of the city’s market values, according to Sweeting, but pay 37.5 percent of all property taxes. Considering that co-ops and condos have sidestepped the bulk of their taxes, the real burden is falling on rental buildings. (Although industrial and commercial properties have it even worse — ”Class 4 is the big loser” in the current tax structure, said Sweeting, since those properties are shouldering 41.4 percent of taxes despite accounting for only 25.7 percent of market value.)

“If the people continue me in office in November, we’re going to put together a process to reform our property tax system,” said Mayor Bill de Blasio on The Brian Lehrer Show in July. His administration has so far sidestepped the issue — a 2014 property tax reform commission called for by City Council Speaker Melissa Mark-Viverito never got out of the gates — but now that de Blasio has won another term in office, what might he take on? There are many potential issues to tackle: Can and should reform be revenue neutral? If policymakers design a system that raises the same amount of money as the current one, there will be winners and losers. Telling some people they will have to pay more has made past reform efforts politically unviable. Will property tax reform focus on the disparities between Class 1 properties to create parity across neighborhoods? Or will it focus on the differences between property types, to counteract the advantage given to homeowners citywide? Regardless, there will be a need for political will in Albany, too — the state legislature is ultimately responsible for any legislative fixes.

What about renters? The burden is largely invisible to renters, who never see a property tax bill. But tenants are shouldering much more than they may realize. Taxes are generally a New York City landlord’s largest expense, accounting for 28.6 percent of operating costs on average according to the Rent Guidelines Board (RGB). Higher property taxes can lead to rent increases or deferred maintenance, even for rent-regulated tenants, since taxes are one factor that the RGB takes into account when determining annual rent increases. (Sweeting cautioned that exactly how much of property tax increases are passed onto renters is an “open question.”) The high property taxes on apartment buildings also likely further incentivize building lower-taxed condos and co-ops instead. Although two-thirds of city residents are renters, there’s another reason that politicians have long been playing property tax hot potato: Homeowners are generally more likely to vote.

The views expressed here are those of the authors only and do not reflect the position of The Architectural League of New York.

Reports from a series of informal conversations with scholars and experts engaging complicated topics in housing policy, hosted by The Architectural League.