We are celebrating 15 years — and counting — of stories that are deeply researched and deeply felt, that build a historical record of what the city has been.

We are celebrating 15 years — and counting — of stories that are deeply researched and deeply felt, that build a historical record of what the city has been.

In New York City neighborhoods where low-income residents face uncertain futures, real estate speculation has become, among other things, a form of information asymmetry. Bankers and investors with access to the means of collecting, analyzing, and acting on proprietary financial data are perpetually one or two (or three) steps ahead of the New Yorkers most likely to be impacted negatively by sudden influxes of new neighborhood investment. And where the profit motive meets a living legacy of housing discrimination, residents at risk of displacement face not only daunting struggles to stay put, but also an often inscrutable mix of law, policy, planning, and finance which obscures the very forces they are up against.

A lack of publicly available information is one of the fundamental imbalances of power in our housing system. But data has also provided, in many instances, the key to tipping this scale. Starting in the 1960s in Chicago, landmark data-gathering efforts aimed at exposing racist real estate practices — byproducts of the now infamous lending policies and practices known as “redlining” — established the foundations for a national movement to disclose mortgage information. These movements, in turn, provided the bedrock for federal legislation aimed at protecting the rights of communities to both access lending data, and to hold lending institutions accountable to community priorities. Gregory Jost carries this history into the present-day Bronx, where for 20 years he has helped community organizations access and leverage data in local struggles for housing justice. Here, he connects historical fights for housing data disclosure across the country to a pressing need for finding ways to follow money through increasingly more complex and global webs of real estate speculation in the 21st century.

Along Southern Boulevard in the South Bronx, a prospective rezoning by the New York City Department of City Planning has concerned neighbors fighting back against looming displacement — but they can’t all agree on whom to target and how to stage this battle. A coalition of nonprofits (including the organization where I work) has pushed for seats at the proverbial table with city agencies and the local councilmember, demanding community control of land and urban planning strategies that prevent displacement of existing residents and businesses. Meanwhile, a more radical group, without ties to traditional funding mechanisms, has adopted an alternative strategy of disrupting the city’s public events and challenging the nonprofits on their participation in a system that drives the rezoning process. While both groups agree that rezonings increase displacement pressures, and that community control and ownership are the best protections, divergent strategies on how to fight City Hall have led to heated divisions within the neighborhood.

One reason for this divide is that City Hall represents only the public face of a much larger problem that we know very little about. Mayor de Blasio has used lofty affordable housing goals to justify a spree of rezonings across all five boroughs. But by changing land use protocols to allow for higher density residential and mixed-use development, primarily in neighborhoods of color, the city also enables a process that enriches developers and investors who profit off the displacement of lower-income communities. The investment is inherently speculative, meaning investors gamble on a neighborhood becoming more valuable through this displacement, with an ideal outcome of gentrification. The money itself, which organizers have labeled “predatory equity,” comes from largely unknown and seemingly bottomless sources, its influence the result of growing economic inequality and wealth disparities in New York and around the globe. Investors, both foreign and domestic, seek a combination of high returns and security, and New York City real estate has performed remarkably well as a financial commodity for the past quarter of a century.

While a rezoning by the city sends a clear message to speculators that another neighborhood is ripe for change, reinforcing the intricate entanglement between our political system and the real estate state, the deeper problem for neighborhoods like Southern Boulevard lies in waves of unregulated speculative investment that are already capitalizing on displacement. The Bronx has become home to many of those already displaced from other boroughs. Even without a rezoning, family homelessness in New York City is at the highest levels since the Great Depression, and many residents live on the edge of eviction every month. If the deeper issue is the power of predatory equity over both land and legislators, those fighting displacement will need to know more about its sources and how it functions to be able to curtail its power.

Beginning fifty years ago, grassroots coalitions fought against a similar predatory real estate practice known as redlining. They won the battle for community-based reinvestment because they were able to first force the disclosure of bank data that proved the structural injustices in the housing and financial markets, and then use that data to win common sense (yet powerful) reforms and enforcement mechanisms that still exist today. Their victories have much to teach those of us currently fighting predatory equity and displacement, especially one crucial lesson: We lack the data we need to identify and expose our targets. We need to know whose money is financing this predatory investment, where that equity is coming from, and what the expected returns are on this investment. It is time we consider the new data we need to frame our campaigns against displacement in the coming years.

Typically, those in power control the means of gathering and distributing data. Tech companies, for instance, are so powerful and profitable because they have learned how to commodify data about the users of their products and platforms. Government and industry leaders also create, access, and control data to build more profitable enterprises, increase efficiency, and maintain influence as necessary. Everyday people, on the other hand, are expected to give up information for some small compensation or convenience, be it access to social media, physical spaces, shopping, or entertainment. To powerfully organize and transform systems, grassroots coalitions have turned this relationship on its head by collecting, analyzing, and presenting data about the injustices of our economic systems. Data is a language that speaks to people, including those in power. Control the data, and you can potentially control the narrative. For instance, if data can show not only a correlation but a causation between racist housing practices and negative outcomes for working-class people, political will and policies can shift dramatically and rapidly.

Beginning in the 1930s, the federal government, through the Home Owners’ Loan Corporation and the Federal Housing Administration, codified pre-existing discriminatory practices of the real estate and financial industries to design a system that either valued or devalued residential neighborhoods across the nation based on explicitly racist ideas. The “infiltration” or “invasion” of “undesirable” people, primarily people of color and immigrants, across real or imagined boundaries, translated into a neighborhood being deemed as a risky investment, cutting off access to low-cost, government-insured mortgage financing, prime-rate insurance policies, and decent municipal services. Real estate speculators quickly realized how to capitalize on the separate and unequal housing markets created by redlining policies, flipping homes and entire neighborhoods in short periods of time using blockbusting and panic peddling techniques to prey both on the racist fears of white homeowners and the desires of Black families to escape overcrowded, already redlined areas for a better life.

Speculators further exploited Black homebuyers through a form of loan sharking known as contract selling, in which Black families took on all the responsibilities of home ownership without the benefits of building equity or security of ownership. Under the system of contract selling, missing one payment meant the home would go back to the seller. Contract buyers were subject to additional, mysterious fees or payment increases, and eviction was a constant threat. But in the summer of 1966, community organizers began door-knocking in the racially changing neighborhood of Lawndale on Chicago’s West Side. They found Black homeowners who, in their desperation to move out of deteriorating redlined neighborhoods, had paid steep prices for their homes only to have billions of dollars of their collective wealth stripped away while having to make impossible choices between taking on multiple jobs, forgoing repairs, or missing a payment and losing everything. The group quickly coalesced into the Contract Buyers League (CBL).

In their growing mobilization against contract selling, the CBL partnered with researchers at Northwestern University’s Center for Urban Affairs. Together, they undertook a massive research project to prove the systemic level of mortgage discrimination against Black families and their neighborhoods that created the conditions for contract selling to thrive. They organized payment strikes and blocked evictions, even moving evicted families back into their homes. They prepared for a large court battle against not just the contract sellers, but also the lending institutions and the Federal Housing Administration who refused to make and insure loans in their neighborhoods. According to Beryl Satter in her historic account of the CBL, exhaustive questionnaires from 475 families supplemented detailed property records for 2,600 plaintiffs and 30,000 complete histories of every property on the West Side connected to a contract selling operation. Organizers and researchers did similar work for the South Side of Chicago, all of it transferred to computer cards and then mapped. The work, often in dingy basements of municipal buildings, was grueling and tedious — one researcher described it as “the sixth rung of hell” — but people knew they were part of something big.[1]

Many factors, including repeated delays and out-of-court settlements, undermined the court case even before it began. When they finally went to trial, the judge ruled the data inadmissible, ironically because it was so compelling. “[The data findings] are misleading. They might be given unnecessary weight, since people feel computers are infallible.”[2] But while the losses were devastating for the families who couldn’t renegotiate their contracts, the data itself had already begun to follow a different path forward.

Meanwhile, a new multiracial coalition was taking shape in Austin, one neighborhood west of Lawndale, where racial change was following a similar pattern of blockbusting, contract selling, and wealth extraction. When Northwestern shared their findings with leaders of the Austin group, local mother-turned-activist Gale Cincotta saw how the underlying issues of neighborhood deterioration were rooted in a similar practice of mortgage redlining. Cincotta believed if they had the data to prove the extent to which banks were taking deposits from neighborhood residents — but refusing to lend that money back out to purchase, refinance, or improve homes or businesses in the same neighborhood — and correlate that data with racial demographics, they could effectively fight back. They pushed the Federal Home Loan Bank of Chicago to release local banking data which showed that in one overwhelmingly Black South Side neighborhood, financial institutions had taken $50 million in deposits but made only $24,000 in mortgages over two years.[3] Cincotta used this data to unite similar neighborhood groups across Chicago, and subsequently the entire country, into National People’s Action. NPA built alliances around everyday issues like sanitation, school overcrowding, and poor housing conditions that all pointed back to redlining as a root cause. In a huge 1974 coalition victory, Mayor Daley announced that the City of Chicago would require all financial institutions holding city deposits to disclose deposit and lending information and pledge to not practice redlining.[4] The coalition leveraged this victory into a statewide disclosure ordinance which passed in the summer of 1975.[5] However, understanding the critical role of the federal government in the mortgage and banking systems, they knew they needed to wage a national campaign.

NPA expanded their fight against redlining by sending organizers along with their monthly newsletter, aptly called Disclosure, to similar neighborhood groups in places like Cincinnati, Cleveland, and Baltimore. In 1974, they came to the Bronx, where they allied with the Northwest Bronx Community and Clergy Coalition (NWBCCC), who had recently formed to fight off the waves of fires and abandonment that had begun in the South Bronx and were spreading north at the rate of ten blocks per year. NPA helped Bronx organizers see how redlining was fueling the infamous fires that ravaged the borough’s tenement buildings, giving hope for a possible solution. It helped that the NWBCCC’s first two organizers were originally from Chicago, where they had been trained in struggles against block busting and contract selling.

By allying with groups like NWBCCC in dozens of states, NPA built a base for its national campaign for a federal mortgage disclosure bill that could prove the vast extent and impact of redlining in neighborhoods across the country. They also found a champion in Wisconsin Senator William Proxmire, the new chair of the Senate Banking Committee. Cincotta sold Proxmire on sponsoring mortgage disclosure legislation, because it didn’t cost the federal government much money, and he was willing to push the banks to do their jobs. By the end of 1975, after an intense legislative battle, the final version of the Home Mortgage Disclosure Act (HMDA) went to President Ford’s desk for signature. The original bill required banks to disclose geographic mortgage lending data including approvals and denials and, to further combat discrimination, the law was updated in the 1980s to include the race, gender, and income of applicants. Armed with HMDA data, NPA groups repeatedly demonstrated the pervasive and systemic nature of redlining and how this practice — not the supposed lawless, pathological, and irredeemable behavior of local residents — led to the deterioration of neighborhoods. Instead of policies of “benign neglect” or “planned shrinkage,” redlined communities required quality lending and reinvestment. Within two years of national mortgage disclosure, NPA won another massive federal legislative victory with the passage of an anti-redlining enforcement mechanism known as the Community Reinvestment Act (CRA).

CRA states that banks have an obligation to meet the credit needs of the communities they serve. While bank regulators control the rulemaking and have made many changes during the past four decades, CRA requires banks to pass tests on lending, service, and investment. Since 1977, community groups have used CRA to challenge discriminatory or insufficient bank practices when institutions apply to their regulators for approval of mergers, acquisitions, or expansions.

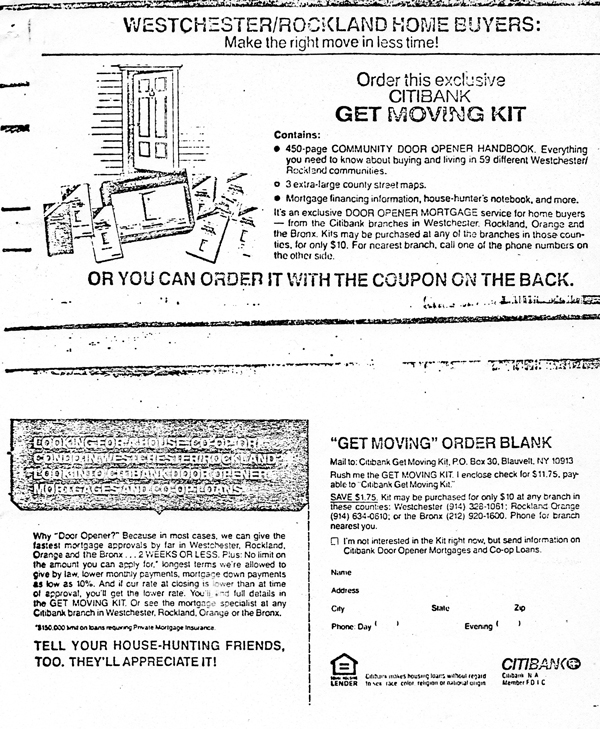

The passage of HMDA and CRA was just the beginning of struggles for investments that truly benefit historically redlined neighborhoods and people. In the early ‘80s, for instance, members of NWBCCC used CRA to challenge Citibank’s plans to open a new Manhattan branch on Park Avenue because the bank had recently closed four Bronx branches, failed to make loans to both private homes and apartment buildings in the Northwest Bronx, and had even sent out a “Get Moving Kit,” encouraging its Bronx customers to apply for mortgages in suburban Westchester and Rockland counties. The challenge led to hearings and a delay of Citibank’s expansion, though the regulator eventually ruled in favor of the bank.[6] Still, HMDA and CRA allow small community organizations to battle giant foes and these laws, with public investment, have created incentives for trillions of dollars to flow into historically redlined neighborhoods.

Yet many advocates feel the laws and rulemaking have not kept up with the larger deregulation of the financial system, and fundamental questions of who benefits from these private investments remain. Blocks have been rebuilt, buildings renovated, and homes improved, but many longtime residents have been displaced, while the racial wealth gap continues to grow. Furthermore, even though redlining was explicitly racist in its logic, CRA is framed as entirely race-neutral, meaning investment can easily evade borrowers of color in gentrifying neighborhoods. In other words, quantifying dollars isn’t enough if we are not able to track the quality of investments and who is building wealth from them.

During the last housing bubble and burst, from 2003 to 2014, research conducted by NWBCCC’s reinvestment affiliate (and my former employer), University Neighborhood Housing Program, documented how sales prices of rent-stabilized Bronx buildings dramatically increased without a corresponding increase in net operating income. Investors were banking either on rising property values to flip buildings for a profit, planning to displace existing tenants to increase rents and cash flow, or both. Since they were not basing their purchase prices on the existing financial situations of buildings, we knew this was speculative investment that sought to do harm to existing tenants one way or another.

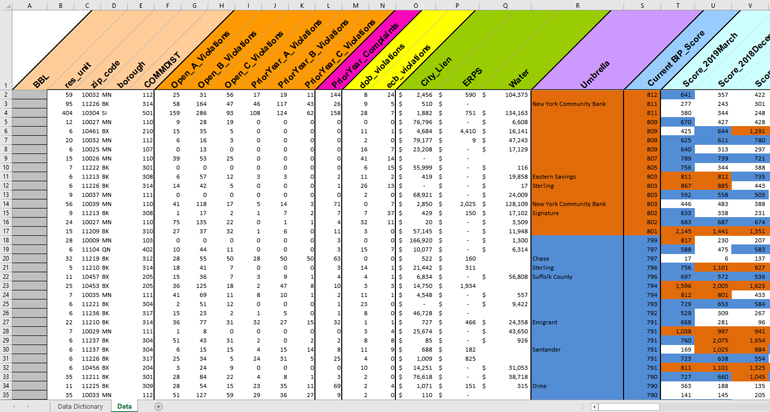

At the same time, the city had begun making property information available through individual building lookups on various department websites. We began to aggregate as much property data as possible to identify any large-scale trends. We pulled data on housing code and building violations, tax and water liens, ownership, management, and — perhaps most crucial for identifying institutional organizing targets — mortgage holder of record. We prototyped a rudimentary scoring system to identify levels of physical and financial distress in Bronx apartment buildings and then called a meeting with a number of prominent multifamily lenders. To their shock, we presented them with our own data on their lending portfolios, with buildings ranked from most likely distressed to least. Many banks pushed back, with one longtime banker confiding, “I don’t want to know this shit,” implying that then he would have to do something about it. That was precisely the idea, and exactly the point of disclosure.

We asked for honest feedback from the bankers about the scoring system and realized any findings were only as good as the data going in. The Giuliani administration had severely cut back on code enforcement and many violations on record were old, while many current violations had gone undocumented. There was no integrity to the violation data until the Bloomberg administration began investing in code enforcement. The more the city did to improve code enforcement, including instituting the 311 hotline system for housing complaints, the better our data became. We targeted our system to capture buildings with more recently issued code violations. In 2006, we subjected our interns to their own “sixth rung of hell” — but instead of sitting in a dingy basement like their counterparts in the 1970s, their eyes blurred scouring numerous city websites, pulling dozens of data fields for over 7,000 Bronx apartment buildings into the first incarnation of the Building Indicator Project (BIP), a database to identify buildings that are likely to be physically and/or financially distressed. By 2008 we semi-automated our system and began pulling records for 60,000 apartment buildings across the city.

Our efforts couldn’t have been timelier. As the housing market began to collapse, many buildings were rapidly deteriorating and going into foreclosure. UNHP worked in tandem with organizers in the Northwest Bronx and around the city to identify and organize buildings that our data predicted to be distressed, increasing efficiency. We continued to meet with the banks to push them to inspect their problem properties and put pressure on landlords to improve conditions. We began sharing data with financial regulators, asking them to use their influence to spur more banks into responsible action with their multifamily borrowers — including delaying refinancing applications until building conditions improved, better screening processes for new borrowers, and overall tighter underwriting standards based on existing rents. We then demanded the regulators use our data to evaluate the banks on their CRA exams, not just for the quantity of lending in our neighborhoods, but also the quality of loans.

Along the way we discovered that many of the distressed mortgages had been sold by the originating banks into commercial mortgage-backed securities, meaning the debt was now owned by anonymous investors around the globe. While we did not have an easy target to hold accountable, we did read through the prospectus documents the securities firms had prepared for investors that clearly stated the intended investment strategies by the landlords. They would “unlock the upside potential” in buildings by pushing long-term tenants out, some claiming a 20 to 30 percent turnover (i.e., displacement) goal in just the first year. When we challenged the banks, who underwrote some of these predatory loans, they defended themselves by saying the investors were putting so much cash and equity into the deal that they still considered their lending conservative. We began to call this type of investment predatory equity, as the cash and equity were specifically designed to push people out of their homes.

One predatory equity group, Milbank Real Estate, had purchased ten buildings across the Bronx, home to more than 500 families. When their gentrification dreams were not realized, they stopped maintenance and allowed living conditions to deteriorate dramatically. We worked closely with organizers and longtime tenant leaders to push the city to be more proactive in intervening with buildings before they became like the Milbank portfolio, where collapsed ceilings, extensive mold growth, peeling paint, long outages of heat and hot water, and apartment flooding became pervasive.

Between the people-power of leaders from the Northwest Bronx and the comprehensive data BIP provided, as well as many legal and advocacy allies, our coalition won the creation of the Proactive Preservation Initiative. The Initiative uses data to preventively target buildings heading toward distress for enforcement mechanisms by the city, and was announced by the Mayor in January 2011. By 2012, all three federal bank regulators were receiving quarterly updates of BIP data, and our research and organizing work pushed the Governor to announce the Slumlord Prevention Guidelines, updating CRA regulations for New York State chartered banks in September 2013. The guidelines provide primarily carrots (and a few sticks) for banks to only lend to landlords “who are committed to the long-term health of a community instead of quick-buck artist slumlords who let buildings fall into disrepair.”

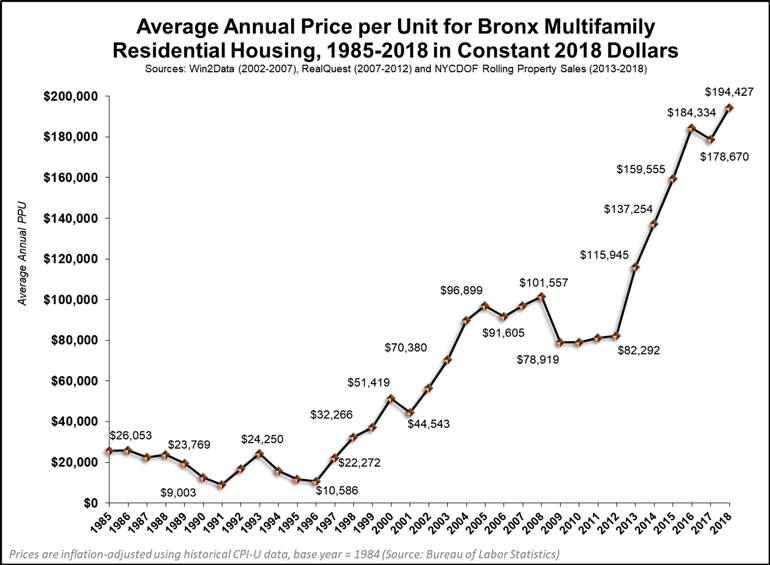

Victories such as these have improved living conditions for millions of New Yorkers, but they have not ended speculative investment, predatory equity, and their offspring: serial displacement and gentrification. Bronx buildings now sell for nearly double what they did at their peak before the market crashed ten years ago, but the median income of Bronx tenants has barely increased. A 25 unit building on Bryant Avenue, in the heart of the Southern Boulevard rezoning area, sold last year for $5.2 million, over $200,000 per apartment. The buyer owns nearly 40 buildings in the Bronx and put in $1.3 million in cash and equity to leverage a $3.9 million mortgage with Country Bank, which has since been refinanced by Santander for $4.65 million. Holding banks accountable to sound underwriting remains critical, but it is insufficient given the amount of cash and equity coming into real estate transactions, as well as the growing alternative of unregulated non-bank lenders who are not accountable to communities at all. Requiring disclosure of cash and equity sources in high-priced real estate transactions, just like banks ask for when a family purchases a home to live in, would shine a bright light onto one of investment capital’s favorite parking lots and laundromats.

In this era of massive wealth inequality, financial deregulation, and an oversupply of global cash and equity, we need to know as much as we can about the money driving real estate speculation to protect our own homes. A small group of researchers, advocates, and organizers have begun to plan a campaign for a state law requiring the disclosure of sources of cash and equity for large real estate transactions — including disclosure of expected returns on that investment. Such a disclosure mechanism could lead to the regulation of non-bank lenders and even investors and their investment vehicles. It could also build support for updating the state banking laws to give regulators more power over banks. Those interested in taking a critical immediate action can submit comments in support of both HMDA and CRA, both of which are currently under attack from Trump-appointed regulators.

These perilous and decisive times call for us to think about the data we need to fight a battle that can seem unwinnable. Without this data, we will likely keep fighting with our neighbors over strategy, dancing around the edges while we all get pushed out of our neighborhoods. As Gale Cincotta would often say during the battle against redlining, where neighbors were often pitted against each other along racial lines, “We’ve found the enemy, and it’s not us!” Just like an earlier generation used mortgage disclosure data to end legal bank redlining, let’s shine the spotlight outward on our true adversaries. The future of Southern Boulevard, the Bronx, and working-class neighborhoods of color across the country hangs in the balance.

Beryl Satter, Family Properties: How the Struggle Over Race and Real Estate Transformed Chicago and Urban America (New York: Picador, 2010), 323.

Satter, Family Properties, 357.

Michael Westgate and Ann-Vick Westgate, Gale Force—Gale Cincotta: The Battles for Disclosure and Community Reinvestment (Education & Resources Group, Incorporated, 2011), 147.

Arthur J. Naparstek and Gale Cincotta, Urban Disinvestment: New Implications for Community Organizations, Research and Public Policy (Washington D.C. and Chicago: National Center for Urban Ethnic Affairs and National Training and Information Center, 1976), 25-26.

Disclosure, July 1975.

Office of the Comptroller of the Currency, Second National Bank Region, transcript of Proceedings, “Application of Citibank, N.A. New York to Establish a Branch at 101 Park Avenue, New York, N.Y., County of New York,” April 20, 1982.

The views expressed here are those of the authors only and do not reflect the position of The Architectural League of New York.